Ask any economist how we should respond to climate change, and they will tell you that the most effective strategy is to put a price on greenhouse gas emissions, ideally through a carbon tax. This reflects a basic economic principle: the waste produced from any activity is a cost that has to be paid. We pay for throwing away our garbage, for cleaning our wastewater, and we should pay for the carbon dioxide waste we create from activities such as burning fossil fuels.

We can put a price on our pollution with a carbon tax or with a cap-and-trade program, as European countries have done for power plants and industry. Cap and trade sets an overall limit on emissions (the cap). Firms with low costs of reducing emissions cut their releases and sell allowances to firms with high costs, which continue emitting, while the set of participants stays within the limit. But prices in cap-and-trade arrangements have proved to be volatile, and the systems need strong oversight to avoid problems.

Why bother? A carbon tax provides greater clarity about the price of emissions, which the business community values. And the U.S. already has a well-developed tax collection system, which works smoothly for collecting excise taxes on many fossil fuels.

For reasons like these, economists such as Gregory Mankiw, former head of the U.S. Council of Economic Advisers under President George W. Bush, have prominently supported a carbon tax. The bipartisan Climate Leadership Council, an international policy institute, published a statement in 2019 that argues that “a carbon tax offers the most cost-effective lever to reduce carbon emissions at the scale and speed that is necessary.” As of this writing, the statement is signed by 3,589 economists—including the three living former chairs of the Federal Reserve, 27 Nobel laureates and 15 former chairs of the Council of Economic Advisers. How the U.S. addresses climate change has become a major topic in the presidential campaign, and there are eight bills in Congress, one with 80 co-sponsors, to put a price on our carbon pollution.

Still, enacting a carbon tax will be a big political lift. If a window does open for it, climate scientists, economists and politicians need to be ready to pounce. They will need to get it right the first time. And they will need to explain why a specific tax rate is justified.

Determining that rate seems to be straightforward: set the tax per ton of CO2 equal to the damage inflicted by its release. But how do we properly assess the damage?

Harm from Emissions

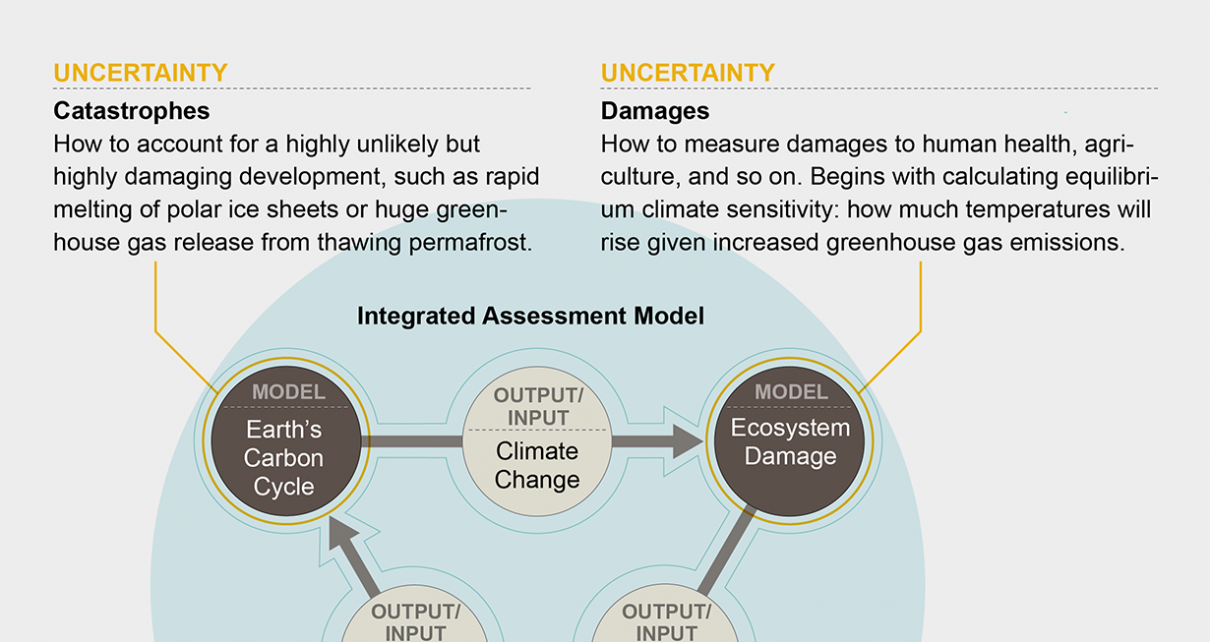

Economists typically calculate climate damages with integrated assessment models (IAMs)—large computer models that capture feedbacks between the economy and the climate. They use a series of equations that characterize the global economy, the worldwide circulation of CO2 emissions arising from economic activity, and damages resulting from atmospheric and upper-ocean temperature increases. IAMs are so important that in 2018 the Nobel Prize in economics was awarded to Yale University economist William D. Nordhaus, for his pioneering work on them.

IAMs such as Nordhaus’s dynamic integrated model of the climate and economy (DICE) have become influential in policy analysis. The Obama administration used three IAMs, including DICE, to determine a dollar value that government should use in cost-benefit analyses for proposed new regulations, including the 2011 tightening of automotive fuel-economy standards.

The models seem to answer the question of how to set the right carbon tax rate. But the damage estimates depend on pinning down several assumptions that have great uncertainty. Three challenges stand out. The first is weighing income today against the income of future generations; for that we need a discount rate, a number that is also important to many policy decisions, such as setting the Social Security tax or funding large infrastructure projects. The second challenge is measuring the damages from our CO2 emissions. Third is how to factor in the possibility of low-probability, high-damage outcomes—so-called catastrophes.

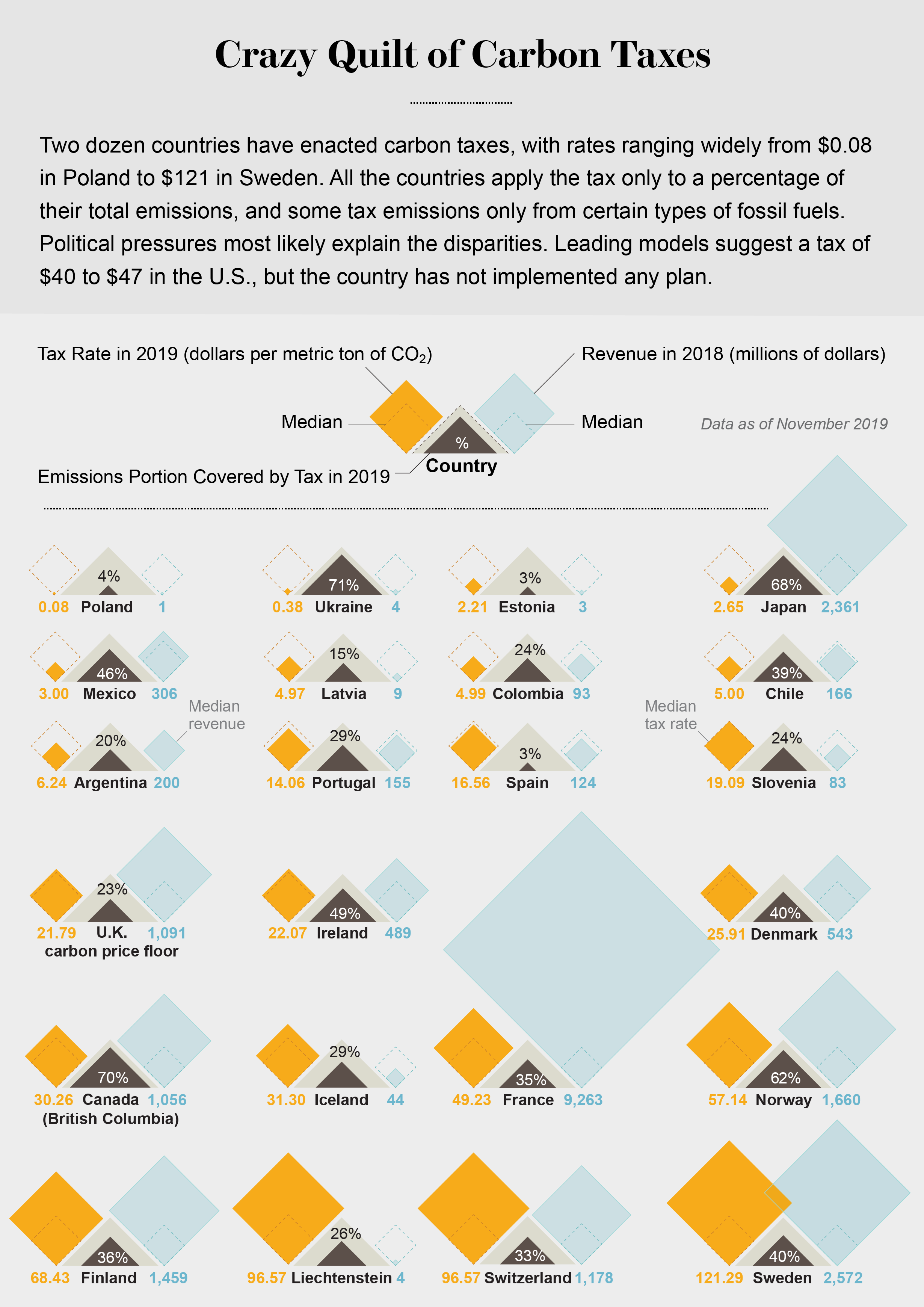

Estimates for the optimal tax rate can vary widely depending on how these factors are treated. In the end, IAMs can give us a solid starting point for a U.S. carbon tax, but the models disagree on the “right” number. Moreover, we have to consider societal and political pressures. Those influences can be huge: 15 European countries have already set carbon taxes, and they range from $2 to $96, with a couple outliers at less than $1 and one at $121.

Social Cost of Carbon

The idea of using a tax to pay for social damages dates back more than 100 years. The influential University of Cambridge economist Arthur C. Pigou maintained that if pollution creates a cost (damage) for someone that is not paid by the polluter, then government should impose a tax on the polluting activity equal to the damages. Pigou, in effect, gave Adam Smith’s so-called invisible hand a green thumb.

Burning one ton of coal, for example, produces roughly two tons of carbon dioxide, by combining carbon atoms with oxygen in the air. If the damages from each ton of carbon dioxide equaled, say, $50, then Pigou’s prescription would be to levy a $100 tax per ton of coal. In that way, the cost of coal would include the cost to society of burning it: the social cost of carbon (SCC). To estimate this cost, we need an IAM. Enter Nordhaus.

Nordhaus published his first paper about the DICE model in 1992. It estimated that in 2015 the SCC would be $4.54 per metric ton of carbon dioxide. When 2015 came around, and after updates to the model, he raised his estimate to $31. Assuming optimal policy, the SCC would grow to just over $100 per ton by 2050 and to $265 by 2100. (All those numbers are in 2010 dollars.)

These estimates are in the middle range among major IAMs. For example, when the Obama administration estimated the SCC for assessing new regulations, it used the DICE model, along with two other well-known models: FUND and PAGE. The 2050 estimates from the FUND model were about half those of the DICE model, and estimates from PAGE were nearly double.

These numbers sound solid, but Massachusetts Institute of Technology economist Robert Pindyck argues that IAMs are useless because they are surrounded by too much uncertainty. His view is extreme, but we do need to take seriously the issues he and others have raised. Let us examine the three key IAM assumptions that can greatly impact the SCC: the discount rate, the damage function and potential catastrophes.

Discounting Future Generations

Any decision involving costs and benefits that are separated in time requires a discount rate. Consider an asset that will pay me $1,000 in 10 years. How much is that asset worth today? Assume I could put some money in an account that pays interest of 3 percent a year. With compounding, $744 invested today would grow to $1,000 in 10 years. In other words, the value of $1,000 in 10 years is $744 today. More precisely, the present discounted value of $1,000 in 10 years is $744, when discounted at 3 percent.

When governments need to choose a discount rate, they sometimes use the return people expect for investing in the marketplace. The U.S. Office of Management and Budget, for example, generally recommends a 7 percent discount rate for assessing government regulations because it is the approximate return on investment in the private sector in recent years.

For long-lived projects, the difference between a 7 percent discount and a 3 percent discount is huge. The present discounted value of $1 million in 250 years is 4.5 cents today at 7 percent. The value is $618 today at 3 percent. The higher the discount rate, the less we should be spending today to reduce future emissions.

Discounting at 7 percent seems reasonable for government projects that last for five to 15 years, but it is not reasonable for climate-related actions, where the benefits from today’s investment could last for 200 years or more. But because people do not typically make 200-year investments, there is no relevant market rate to go by. That is true even for government-led infrastructure investments. Most of these projects, for example, the Erie Canal, have useful lives of 50 to 100 years before they need to be rebuilt or are abandoned because of innovation—in the canal’s case, by railroads, then highways.

If market rates are not a good guide, perhaps we can use economic theory. Economist Frank Ramsey, a peer of Pigou, argued that the discount rate for long-term outlooks should take into account two considerations. The first reflects an ethical decision about how to treat different generations. This leans toward a low discount rate, on the grounds that we should not treat future generations differently than we do our own. Second, the discount rate should take into account changes in income over time; the richer future generations are compared to us, the less we should feel compelled to incur costs now to make them better off. That leans toward a high discount rate.

In 2006 British economist Nicholas Stern wrote a review of climate change for the U.K. government, taking both these factors into account. His so-called Stern Review concluded that the correct discount rate for climate policy was 1.4 percent. At that rate, $1 million in 250 years is worth nearly $31,000 today, far more than the $618 calculated using a 3 percent discount rate. Given his calculations, Stern argued that the costs of climate change were five times the costs of cutting emissions. The Stern Review was highly influential around the world in shaping the narrative about the need to make dramatic and rapid reductions in emissions now.

As a practical matter, we have to square approaches that lead to high and low discount rates. One resolution is that a discount rate should not remain constant over time; it should decline. If uncertainty about future income grows greater the further we go into the future, for example, then we need a precautionary factor. The late Harvard University economist Martin Weitzman argued that a discount rate of 4 percent should be used in the near term, whereas 1 percent should be used for the distant future (76 to 300 years), with a gradual decline for time periods in between.

In the end, economists do not have clear guidance on the “best” discount rate, in part because of the ethical choices involved across generations. Small changes in the discount rate, however, can lead to large changes in the SCC—an important factor in setting a carbon tax.

Uncertain Damage

The second uncertainty in setting a price on carbon is the damage CO2 emissions will impose on the economy. In the DICE model, damages are, roughly speaking, a function of the square of the temperature increase. This approach is a shorthand for the complex impacts of warming, such as lower agricultural productivity, higher death rates from heat and diseases, loss of species, geopolitical risks such as drought-driven human migrations, and so on.

Nordhaus, like other IAM modelers, based his damage function on a review of the existing literature. This is good news because scientists have made great progress in measuring the damages from climate change. But no one can capture all possible injury. To compensate, Nordhaus increased his damage estimates by one quarter. His function leads to worldwide damages equal to 8.5 percent of global income for a planetary temperature increase of six degrees Celsius. In contrast, U.S. gross domestic product fell by more than 25 percent during the Great Depression from 1929 to 1933.

Scientists have a way to quantify the likelihood of a big temperature rise. In 1896 Swedish chemist Svante Arrhenius used a series of detailed measurements to estimate that doubling the atmospheric CO2 concentration would warm Earth by four degrees C. This relation, now known as the equilibrium climate sensitivity, has proved remarkably durable. Unfortunately, little progress has been made in narrowing the uncertainty around it. The Intergovernmental Panel on Climate Change’s Fifth Assessment Report (the most recent) states that equilibrium climate sensitivity is “likely in the range 1.5°C to 4.5°C, extremely unlikely less than 1°C, and very unlikely greater than 6°C.” But the swing in damages between 1.5°C and 4.5°C is huge. IAM modelers can deal with this kind of uncertainty by making thousands of model runs, varying key parameters. They then report central estimates, and upper and lower bounds, to give policy makers a sense of the uncertainty around SCC values.

This is not entirely satisfactory. Weitzman said there is a “worrisome amount of probability” that equilibrium climate sensitivity could be above 4.5 degrees C. This enters the realm of extreme consequences.

The Price of Catastrophes

Catastrophes are low-probability, high-damage events. Weitzman cited a long litany of the “known unknowns” that could lead to catastrophes, such as rapid sea-level rise from quick melting of the Greenland and West Antarctic ice sheets or from significant changes in ocean-circulation patterns. He also considered “unknown unknowns,” such as runaway climate feedbacks we have not yet identified. One example might be that warming thaws all permafrost on Earth, which releases huge amounts of CO2 and methane, creating runaway heating. This is not just academic talk. Investment firm JPMorgan Chase recently released a report to bank clients that warns, “We cannot rule out catastrophic outcomes where human life as we know it is threatened.”

On a graph, a normal distribution of the likely rise in temperature would look like a hump: a low tail at the left (unlikely), leading to a high hump in the middle (most likely), and a low tail on the right (unlikely). As our knowledge improves about how the climate is responding to our emissions, we can refine this distribution. It appears that the distribution will be “fat-tailed,” meaning the probability of very large temperature increases (the tail to the right) goes to zero more slowly than in a normal distribution. This creates a fundamental problem for IAMs, which Weitzman called the Dismal Theorem: society should be willing to pay an infinite amount to avoid low-probability, high-damage events because expected damages are infinite. Clearly, society cannot do that.

Weitzman was not quite sure what to make of his theorem. He argued that researchers should focus more on understanding catastrophic events, to reduce our uncertainty about their likelihood and consequences. That knowledge can better inform policy choices required to respond appropriately to possible catastrophes.

How to Proceed

In the meantime, we need to determine the SCC and carbon tax rate. Uncertainties about the discount rate, damages, climate sensitivity and possible catastrophes mean that any estimate of the SCC is uncertain. The only thing we can say for sure is that the SCC must be greater than zero; any pollutant incurs a cost. It is heartening to see greater collaboration between economists and scientists—signaled by the science journal Nature appointing an economics editor—because it will lessen such uncertainties.

For policy makers, IAMs can provide a starting point for setting a schedule of carbon tax rates for the next few decades. For example, the three models the U.S. government used in 2016 for analyzing potential regulations gave a range of estimates for the SCC in 2020. Assuming a 3 percent discount rate, Nordhaus’s DICE model suggested a mean 2020 tax rate of $47 per metric ton of carbon dioxide. Mean estimates from the other two models were $23 and $84.

Nordhaus’s rate is very close to the $40 per ton rate suggested by the Climate Leadership Council. It is also close to the average initial tax rate in the seven carbon tax bills filed in Congress. In its base case, the council’s tax rate would increase 5 percent each year, leading to a tax of $65 in 2030 and $173 in 2050. An economic model from Stanford University and Resources for the Future suggests that the Climate Leadership Council’s proposal would create an immediate 18 percent reduction in emissions and a 50 percent reduction by 2035, relative to a U.S. economy without a carbon price. This would put the country well on track to becoming carbon-free by midcentury.

The tax would also generate a lot of revenue for the federal government. A U.S. Treasury study estimated that a carbon tax of this magnitude would raise more than $1.5 trillion over the next decade, after accounting for losses in business and related tax revenues from the tax. Focusing on revenue is a fiscal argument for a tax that might appeal to congressional policy makers who, at some point, will need funds to close a spiraling budget deficit. Or the revenue could pay for some of the zero-carbon infrastructure called for in the Green New Deal. Such an approach focuses on a carbon tax’s role as a fiscal instrument more than as an environmental instrument. The government could also give carbon tax revenues back to households through a “carbon dividend,” as the Climate Leadership Council has proposed.

A different strategy would focus on emissions reductions, not revenue potential. After all, taxing CO2 will not actually guarantee a given emissions reduction, even though raising the cost of emissions will definitely drive them down. Economists, for example, have run a model of the U.S. economy that indicates a $43 tax per ton starting in 2019 would have been sufficient for the U.S. to meet the Paris Agreement goal of a 28 percent emissions reduction by 2025.

Alternatively, a carbon tax could be viewed purely as an insurance policy against catastrophes. The tax would not eliminate the risk but would help reduce it. We could call this the Grand Canyon effect. If I stand at the edge of the Grand Canyon taking in the view, there is a risk that a sudden wind gust could cause me to lose my balance and fall over the edge. By taking a step back, I reduce that risk. By slowing the rate of emissions, we reduce the risk of a catastrophic climate event.

A hybrid approach would set a tax on CO2 and periodically update the tax rate depending on how much progress the U.S. is making toward reducing emissions. But updating is problematic. Enacting a carbon tax is going to be a political fight for Congress. Once done, Congress is unlikely to have the appetite to periodically reopen the debate by reviewing and adjusting tax schedules. We can get around that by including a “policy thermostat” in the initial legislation. For example, the legislation could include explicit emissions-reduction targets over 10 and 20 years and a process for adjusting the tax rates automatically if the country is not on track to hit those targets. A number of the U.S. carbon tax proposals use this approach.

If the U.S. moves forward with a carbon tax, it has to consider important design issues: What to do with the tax revenue. What to do for workers in carbon-intensive sectors of the economy. How to incentivize carbon capture and sequestration. Whether to tax the carbon dioxide embedded in imported goods. And whether there is a political trade-off to be had in relaxing some environmental regulations in return for a carbon tax.

Additional policies will be needed, too. Certain greenhouse gas sources may not be amenable to taxation and might be more cost-effectively addressed through regulation. One example is methane emissions from oil and gas fields. Trying to measure and tax them is unrealistic; requiring technologies that reduce the leakage is more effective. More fundamentally, we will need more funding for R&D to invent and bring to market affordable zero-carbon energy technologies and perhaps cost-effective carbon capture and storage technologies.

Putting a price on our emissions now is essential. Here is a simple reason why: 2019 was the second hottest year on record worldwide, and the past five years were the hottest of the past 140.